What is Superannuation | How Super Works

Superannuation, popularly known as “Super” in Australia is the primary source of retirement savings for salaried Aussies.

Every pay cycle, your employer is obligated by law to contribute a fixed percentage of your overall pay to your Super/retirement fund. Maybe you are starting your first job and not sure what it means to have a super. This guide will help you dive into the nitty-gritty’s of the subject.

Let us start with a brief history of retirement funds in Australia before we dive into the details of the modern Australian Superannuation Guarantee (SG) system.

History of Superannuation

Pension or retirement plans have a rich history of existence. Initially popularized as a safety net for retired military persons in their older age.

It was not until the 18th century that Germany made it compulsory for all government institutions to set up a retirement plan for their employees.

In Australia, the origins of the system date back to the late 19th century. In 1908, NSW was the first state to announce a set rate of 26 pounds per year, in an attempt to keep individuals in modest comfort upon retirement.

The most significant legislative changes that affected pension rates have been the introduction of indexation in the1930s, the introduction in the 1960s of different rates of pensions for singles and couples and legislating the minimum Superannuation Guarantee in 1992.

On 21 August 1991, the then Treasurer, John Kerin, announced a new system to be known as the Superannuation Guarantee (SG), where employers would be required to make superannuation contributions on behalf of their employees.

If the required amount of superannuation support was not provided, the employer would be liable for a non-deductible Superannuation Guarantee Charge. The SG system suggested by Kerin is still in place to help meet the challenges of Australia’s aging population.

What is Superannuation

Simply superannuation is a small portion (10.5% as of 2023) taken off every paycheck from your salary and pecked away for your retirement.

These monies are invested in stocks, bonds, and funds managed by experts to grow over time and yield significant compounding for your retirement.

This system ensures that by the time you retire, you have accumulated enough savings to support yourself, along with any government-provided age pension.

What is a Super Fund

A super fund is a professional financial institution that holds and invests your super savings.

A few of the popular funds in Australia are UniSuper, Hotplus, HESTA, AustralianSuper, Australian Retirement Trust, and Active Super.

Normally if you are starting your first job, your employer might start paying your super contributions towards their preferred standard super fund. However, you have control over the decision of which fund to choose.

It is advisable to choose your preferred Super fund based on the following factors:

Fee

Super funds are mostly managed by big private conglomerates. And like any other financial institution, they charge a fee. They have different fee structures. It could either be fixed or a percentage of your investments. Generally, the lower the fee, the better. And generally, a low monthly fixed fee is better than a percentage.

Performance

It is best to compare the past few years of performance of your choice of fund. “Past performance is not an indicator of future performance” is a quote massively popularized in the finance industry. However, it is a good way to ensure you have your savings invested in a fund that had positive yields over the past years.

Investment Options

Mostly every super will let you choose from a range of investment options. You can choose from multiple investment options depending on your risk tolerance. Usually in the range of growth(Med-high risk), balanced (equivalent to inflation/GDP growth rate), and conservative (Low risk). Not financial advice, but if you are young, going with a growth investment option could be a preferred choice.

Ethos

Ethical investing has grown big recently. More and more Millennials and Gen Z flood the work environment. Financial institutions have observed a shift from more profit-driven investing to ethical investing. You can select a super based on their investment ethos and values.

How Does Your Super Work

So far, we have established what a super is and the mechanisms behind the system. What happens once your money is put in a super?

Let us dive into that.

A few things you need to understand to know how your super grows.

What Are Super Contributions

A super contribution is the amount that is put towards your super fund every pay cycle.

It can be done in a few different ways, let’s understand what are the different options you can contribute to your super

1- Compulsory Employer Contributions

As the name suggests these are the compulsory contributions made by the employer towards your Superannuation guarantee (SG). Currently, sitting at 10.5% of your ordinary earnings. This rate is subject to increase periodically as legislation changes.

2- Voluntary Concessional Contributions – Salary Sacrifice

The Australian government provides tax concessions to those interested in making additional contributions towards their super. Concession is usually provided by availing a lower tax rate of 15% on the contribution.

Voluntary concessional contributions can be made by arranging them with your employer. They are made from your pre-tax income. Hence, also known as Salary Sacrifice.

Once agreement is in place, your employer can contribute a set amount from each pay cycle towards your super fund. Helping you in contributing more towards your retirement fund.

3- Voluntary Non-Concessional Contributions

Currently, Capped at $110,000 per year. These are the funds that you can contribute from your after-tax income. As the tax is already paid on the income, these contributions are not subjected to any further superannuation tax.

4- Spouse Contribution

To promote retirement savings, the government provides a great option for low earning households. If your partner earns less than a threshold income, a super contribution to their fund can provide you with additional tax offsets.

How is Super Taxed

The big O moment if you haven’t considered it yet. Your super is not tax-free. The big O moment if you haven’t considered it yet. Your super is not tax-free.

Both your super contributions, and investment earnings are taxed at a flat rate of 15%. Which is lower than the marginal rate of tax in Australia.

Moreover, Non-concessional contributions are deemed for no further taxation, as they are made with after-tax income. Therefore, capped to a certain dollar amount.

How Does a Super Grow

Just like any other financial instrument out there. Your super is primarily a financial product you invest into.

Your contributions are invested into various assets like stocks, bonds, and property. It entirely depends on your choice of Superfund and investment options available to you. Any factors that would affect the prices of these assets directly impact the growth of your super fund.

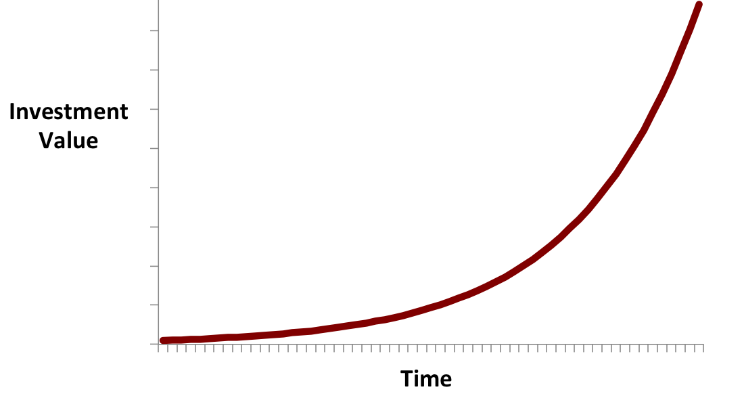

Understanding the Compound Effect

The concept of compounding popularized by the likes of Darren Hardy, Warren Buffet, and Charlie Munger can be really helpful in understanding the factors behind the growth of your super.

Your super will not grow in 1 month or 10 years, it is the matter of compounding small wins that will eventually give you that big fat reward at the time of your retirement.

A few things you need to understand for maximum growth over the life of your fund.

1- Small Choices Matter – Every contribution matters, and savings in fees matter.

2- Momentum builds with time – Growth is exponential, and it might be insignificant in the start until your funds start gathering that momentum

3- Tracking matters – You need to regularly review your investment options to ensure your performance is in the right direction.

How can you access your Super

Except for a few specific conditions you cannot access amounts in your Super fund until you reach your retirement (preservation age).

Early access may result in a high tax rate on your amount withdrawn depending on the reason for withdrawal and total amount withdrawn.

You can look up more details about this.

Not a financial advice:

Just a caution to yield maximum out of compounding it is highly advisable not to touch your super savings until you reach retirement age. It will negatively impact your growth and overall pension withdrawal when retired.

How to keep track of your Super

As an Accountant who happened to have assisted numerous clients with their super. It is advisable to regularly check how your investments are performing, and may be making a change or two as needed to ensure overall positive returns during the lifetime of your super fund.

With the advent of modern tech, it is now much easier to keep an eye on the performance of your superannuation funds. Many popular Super companies now provide options such as apps, and web-based portals to regularly track & review your fund’s performance.

Staying updated with the changes in legislation and financial landscape is another great way to make sure your chosen investment options are working for your best interest, rather than the that of financial institutions.

My 2 Cents

The Australian government encourages individuals to take control of their finances. There’s heaps of support and help available in the form of free educational resources, online portals, and experts to help you make the best decision for your super.

Understanding and managing your superannuation effectively can make a significant difference to your life in retirement. The best way to do this is to learn and equip yourself with the essential knowledge and follow credible sources like ours to always stay up to date with the latest in the industry.

Qualified CPA, with a background in accounting and finance, I bring a wealth of knowledge and experience to My Tax Daily. Having worked with diverse clients across various industries, I understand the intricacies of individual tax laws and regulations. My commitment to making complex tax information accessible and understandable for everyone drives my writing. My content is rich in expert tips and latest tax information, curated to simplify your financial and taxation affairs.

One Comment